Amid a backdrop of global uncertainty and turmoil in international trading conditions, data of business and consumer confidence were bleak for this quarter. There was a sharp uptick in inflation in April although this is expected to be a one-off jump caused by regulatory decisions on the prices of water and energy bills.

And the UK recorded the highest quarterly GDP growth of anywhere in the G7 – although this might come at the expense of growth later in the year.

Businesses have slowed hiring as the impact of the increase in National Insurance contributions makes its mark on the labour market.

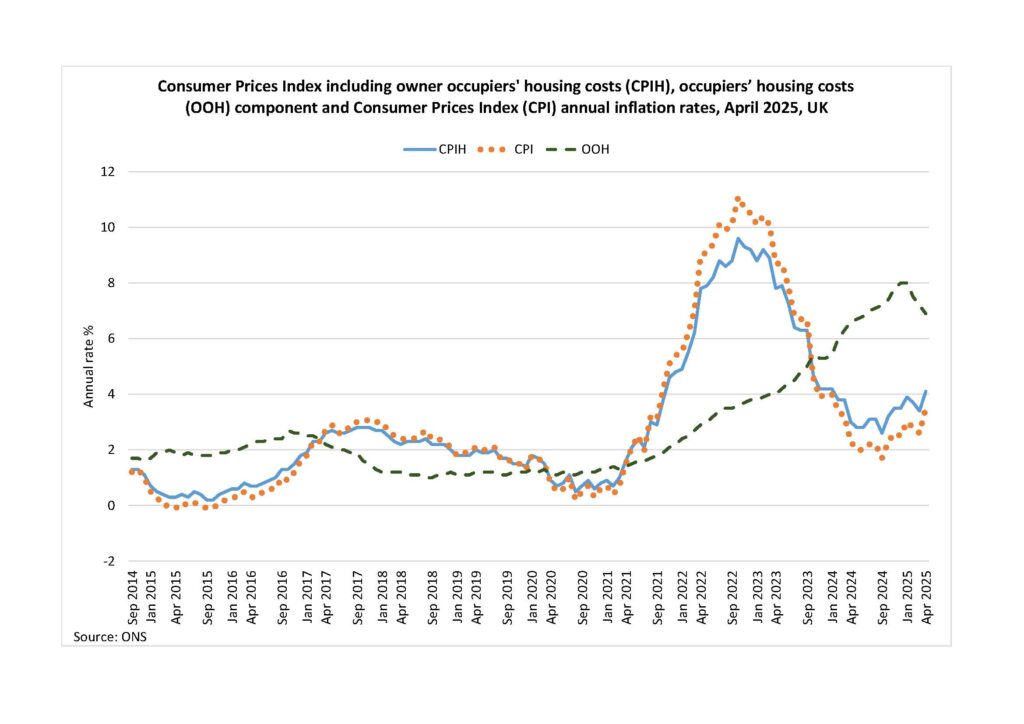

The UK rate of inflation, measured on both a 12-month rate and month-on-month, rose sharply in April. On the measure that includes housing costs (CPIH), inflation rose by 4.1 per cent in the 12 months to April, up from 3.4 per cent in the 12 months to March, and by 1.2 per cent compared to the previous month.

Excluding housing costs, the Consumer Price Inflation rate (CPI) accelerated to 3.5 per cent in the 12 months to April, compared to 2.6 per cent in March, and there was a monthly increase of 1.2 per cent.

The most significant contribution to upwards inflationary pressure came from housing and household services, where annual inflation was 7 per cent in April compared to 5.1 per cent in March. A large increase in the regulated prices of utilities in part explains this spike.

The cost of household energy rose as the Ofgem energy price cap for the period between April and June rose by 6 per cent, to an annual average equivalent of £1,849, up £111 over a year. On top of this regulators have raised the price of water and sewerage, which rose by 26.1 per cent in April, compared to March – this was the largest monthly increase since February 1988.

The cost of owning or renting a house is still rising but at a slowing rate. In Scotland house prices increased 4.6 per cent in the 12 months to March, down on February (5.3 per cent) and at a slower rate than the UK average increase (6.4 per cent). The average price for a house in Scotland is now £186,000 compared to £271,000 in the UK.

Private rents averaged £999 in Scotland in April, an increase of 5.1 per cent on the year, slightly slower than the 12 months to March. Across the UK, monthly rents increased by 7.4 per cent in the 12 months to April, also reflecting a marginal slow down. Data for Scotland reflects mainly advertised new lets so comparisons with the UK should be made with caution.

In May, the Monetary Policy Committee cut interest rates by a quarter of a per cent to 4.25 per cent, the fourth cut since the summer of last year. The temporary nature of the factors driving recent inflation means that the Bank of England is confident that CPI will fall back close to the 2 per cent target by the end of next year, with the peak annual rate of 3.7 per cent expected in September.

Consumer worries about prospects

After turning negative in the second half of 2024, the Scottish Consumer Sentiment Index (development data) declined to -6.5 in the first three months of 2025, a fall of 1.6 compared to the previous quarter. Weakening expectations for the future performance of both the Scottish economy as a whole and household finances were the main drivers of the fall.Despite the bleak mood expressed in consumer surveys, Scottish shoppers took advantage of the sunny weather making April 2025 the best monthly retail performance for almost two years. Total Scottish sales were up by 4.6 per cent on the year (adjusted for inflation) and footfall increased by 6.9 per cent. However, this also reflects the later timing of Easter compared to last year and followed a difficult March where footfall was down by 6.9 per cent.

Scottish shoppers took advantage of the sunny weather in April

Business activity in Scotland falls sharply

ncreasing domestic costs and global uncertainty continue to create headwinds for businesses. The Royal Bank of Scotland regional growth tracker, an index which measures the month-on-month change in manufacturing and service output (a score above 50 means month-on-month growth, below 50 a contraction)

dropped to 45.9 in March, from 49 in February.

This was the sharpest monthly fall since November 2022 and put Scotland second last across UK regions and nations. Market uncertainty and budget constraints were given as reasons for lower levels of new orders that have fallen for six consecutive months.

Firms responding to the Fraser of Allander Institute (FAI) Scottish business monitor in the first quarter of 2025 were more pessimistic about the economy. All survey measures – including business activity, employment, capital investment, and exporting – were negative for the second consecutive quarter.

The FSB small business index score for Scotland increased to -15.3 in the first quarter of 2025. Although that means more Scottish small businesses expect performance to worsen rather than improve over the coming quarter, this was a significant improvement on the previous quarter and is better than the UK score of -40.7.

{kind=link}