Scotland’s farms, fisheries and forests are facing mounting pressure from all sides – and the result is likely to be a significant increase in food inflation later this year

Scotland’s rural economy is not a sideshow; it is critical to our national resilience. But it is being squeezed from all sides: by global shocks, rising energy costs and domestic policy choices that add further strain.

Food, and the price of it, took centre stage in the recent Scottish Parliament election campaign. The SNP’s controversial manifesto commitment to cap the price of certain food staples such as bread, milk and eggs prompted strong debate as how to best shield consumers from rising costs.

Scotland’s farms, fisheries and forests link directly to consumers at home and across global markets. The question of who bears the cost – producer or consumer – now sits at the heart of a story shaped by mounting pressures.

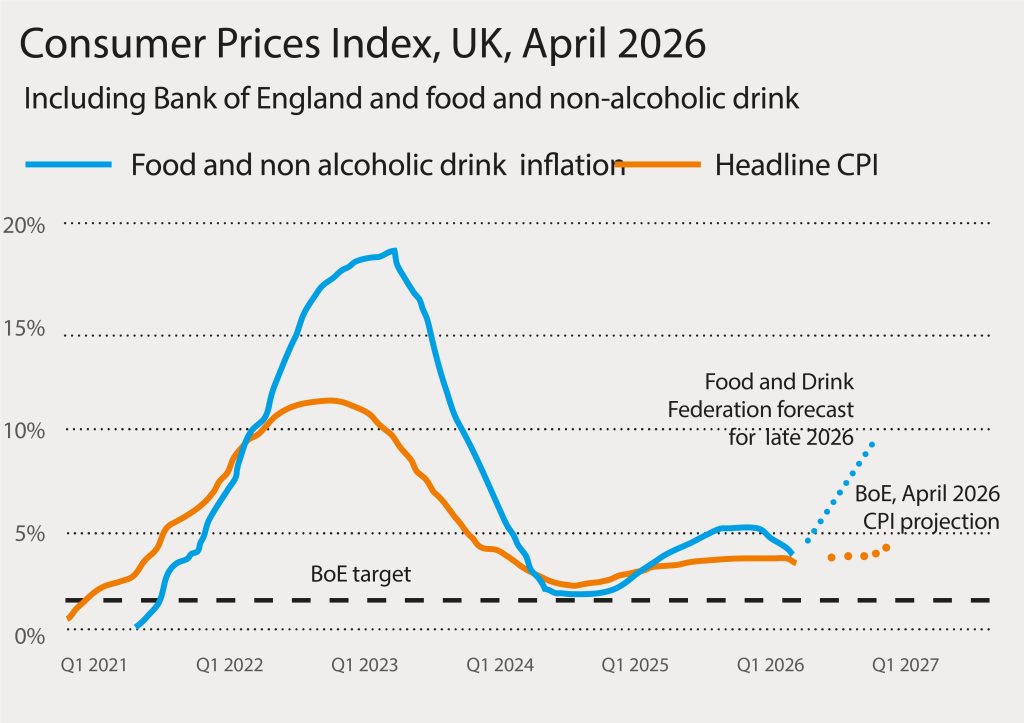

Inflation, as measured by the Consumer Price Index (CPI), largely cooled over the first quarter of the year, with prices rising by 2.8 per cent in the 12 months to April (the lowest rate since March 2025). But the outbreak of armed conflict in the Gulf from late February will result in a drastically changed position by the end of 2026.

The Bank of England forecast from April estimates that CPI will rise to 3.3 per cent by the third quarter of this year – up from the 1.9 per cent forecast only in February. Motorists have already noticed how much more it costs to fill up at the pumps, with the price of a litre of petrol increasing by 16.6p in April compared to the previous month and diesel rising by 31.3p.

Rural businesses will be particularly hard hit, with food and drink manufacturing being energy intensive and subject to prices set by global commodity markets. For example, the price of red diesel (used for powering agricultural machinery) rose by 78 per cent in the first ten days of hostilities between the US, Israel and Iran.

Heating oil, predominantly used by households living off the national gas grid in rural areas, more than doubled in the first week of conflict. As of late May, red diesel and heating oil prices were still 50 per cent higher than prior to the war. Most other households will be on Ofgem’s default energy price cap, which will increase to £1,663 (on an annualised basis) for the third quarter of this year, a rise of 13 per cent.

The Food and Drink Federation (FDF), the sector’s trade association, has forecast that food inflation will reach at least nine per cent by December – a significant upward revision to its forecast of 3.2 per cent from September 2025.

This would be the highest increase in food and non-alcoholic drink prices over the course of a single year since the inflation shock following the Russian invasion of Ukraine in February 2022.

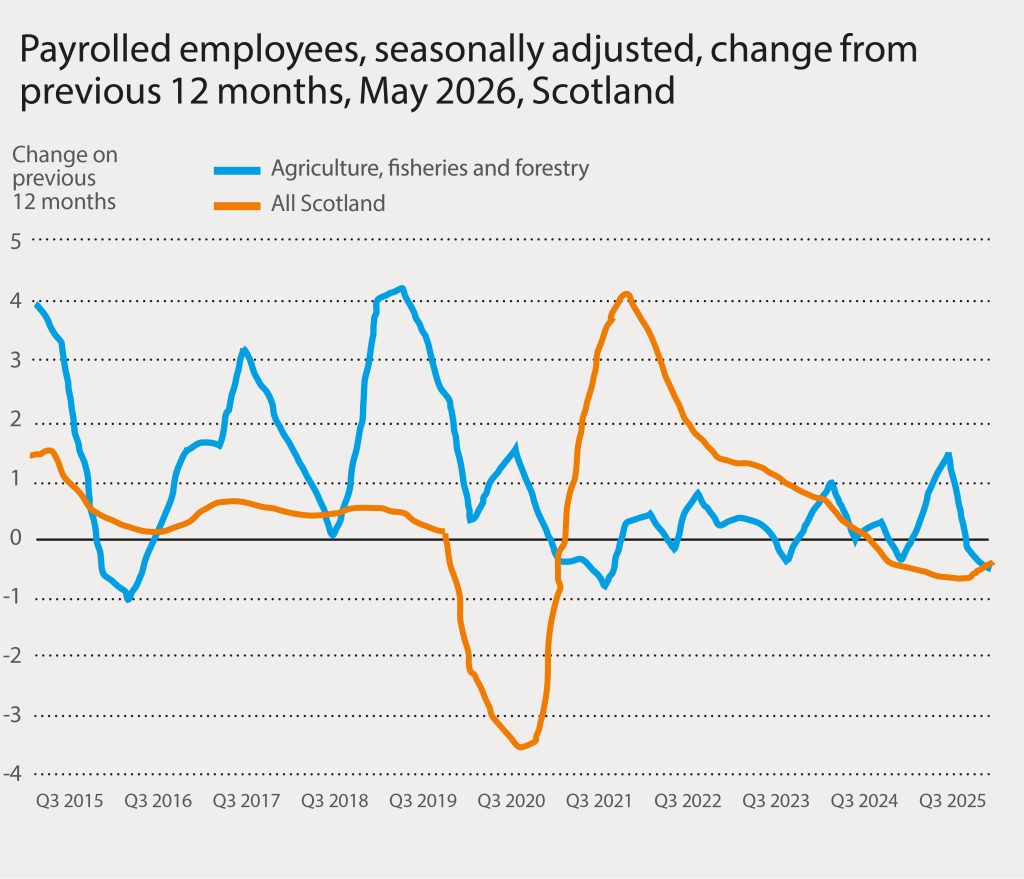

Perhaps a symbolic indication of the headwinds facing Scotland’s rural economy has been the reduction, by 1.5 per cent, in the payrolled workforce (which doesn’t include self-employed workers or contractors) in the agricultural, fisheries and forestry sector over the 12 months to April.

That is slightly higher than the reduction in employee headcount in the sector at UK level (1.1 per cent) and across the Scottish economy as a whole (0.6 per cent).

The rural economy has a particular economic and social importance to Scotland. While the country makes up only eight per cent of all UK workers on company payrolls, it accounts for 13 per cent of payrolled employees in the agriculture, fisheries and forestry. That makes the challenges facing the sector, especially falling employment, particularly concerning from a Scottish perspective.

While the rural jobs market would appear to be softening, wages have held up. Median monthly pay in the sector in Scotland stood at £2,596 in April, a rise of 4.8 per cent on the previous year. This is higher than average at the UK level (£2,382) but slightly lower than employee wages across all sectors in Scotland (£2,659).

In recent years, many firms have reported in surveys such as the Scottish Business Monitor, run by the Fraser of Allander Institute (FAI) at Strathclyde University, that employee payrolls were a major driver of cost pressures.

However, the FAI’s survey from the first quarter of 2026 found some easing of employer concerns on staff costs. Instead, energy costs have become the dominant pressure for firms: 79.2 per cent of respondents reported higher energy bills in the first three months of this year and 89.4 per cent anticipate further increases in the next six months.

Although the geopolitical situation has contributed to inflationary pressures in many countries, recent decisions made by governments at Westminster and Holyrood have imposed additional costs on food and drink producers, which in turn have been passed onto customers.

The rise in employer’s national insurance, increases to the national living wage, the employment rights act, business rates and the deposit return scheme have all inflated costs for farmers, manufacturers and retailers.

If politicians are serious about driving down grocery costs, they should avoid making interventions that add costs to businesses

If politicians are serious about driving down the price of a basket of groceries, then they should avoid making policy interventions that add costs and complexity to businesses. Farmers and food and drink manufacturers often operate on narrow margins, meaning additional costs are usually passed directly onto consumers.

This passing on of price increases has an impact on other sectors in the rest of the economy. In April, roughly equal numbers of firms responding to the business insights and conditions in Scotland survey reported that the cost of inputs had stayed the same (40.5 per cent) rather than increased (39 per cent).

That is a sharp contrast from February, when more than twice the number of businesses said input prices remained unchanged compared to the previous month (55.2 per cent) compared to those which reported increases (24.2 per cent).

Consumer confidence fell sharply in March as the Middle East war dominated news headlines. In the first two months of the year, marginally more respondents to the Scottish consumer sentiment indicator expected that prospects for the Scottish economy and household finances would improve.

But in March, 31.7 per cent of respondents thought that the performance of the Scottish economy would worsen over the coming 12 months (22.4 per cent believed it would improve) and 32.9 per cent thought that household finances would weaken over the next year (compared to 22.9 per cent who said it would improve).

Rising costs and falling consumer demands would explain why the hotels, restaurants and catering sector was the UK’s weakest-performing industry in the first three months of 2026. According to the RBS Regional Growth Tracker from March, business activity in the sector fell at the lowest rate since the height of covid restrictions in the first quarter of 2021.

The sector had the highest number of job losses, according to data in the survey, at a rate not seen since the pandemic. Administrative data from HMRC showed a 3.5 per cent reduction in payroll headcount in accommodation and food services firms in Scotland in the 12 months to April.

Notwithstanding the difficult picture on inflation and the bleak mood indicated in survey data, the UK economy grew by 0.6 per cent from January to March this year; the highest growth in the G7 in the first quarter. Production, services and construction all grew, which defied the expectations of many economic commentators and suggests some underlying resilience in the economy.

However, this data only gives a snapshot of what has happened in the past. A prolonged period of heightened geopolitical instability in the Gulf (even if military hostilities are suspended) will have a significant economic impact at home.

In March, the Organisation for Economic Co-operation and Development, an international forum of mostly developed countries, lowered its 2026 forecast for UK GDP from 1.2 per cent to 0.7 per cent and raised its forecast for UK inflation from 2.5 per cent to 4 per cent.

In Scotland, GDP grew by a more modest 0.1 per cent in the first quarter. Although output in services and construction both expanded, there was a contraction of 0.7 per cent the agricultural, fisheries and forestry sector. Compared to a year ago, the sectors which make up the bulk of Scotland’s rural economy are 3 per cent smaller in size.

These figures make for a rather forlorn reading. But it is too easy to become disheartened. Although the UK has, yet again, found itself badly exposed to events overseas, the disruption to supply chains caused by the closure of the Strait of Hormuz illustrates the vital importance of domestic production of essential supplies, especially food.

Perhaps that might offer a crumb of comfort to Scotland’s farmers, landowners and food producers this summer.

Join The Business at the Royal Highland Show, an annual event, showcasing the best of food, farming and rural life at Ingliston in Edinburgh. Thursday 18 – Sunday 21 June, 2026.

Read more from our Royal Highland Show 2026 section here.

Prosper.scot is a cross-sector economic alliance that aims to

strengthen Scotland’s economy.