The January sales delivered a boost to the economy, but business activity and confidence are falling ahead of wage increases and global concerns over President Trump’s tariffs.

Inflationary forces are building again across the economy with upwards pressure from VAT on school fees, transport, food and drink despite a fall in energy costs for households.

Growth remains weak across the UK with private sector business activity declining in Scotland for a second quarter, and a further loosening in labour market conditions.

Businesses are concerned about rising costs ahead of the introduction of the increase in National Insurance Contributions in April. And despite a strong retail performance in the January sales, weaker consumer sentiment about the economy and personal finances suggests this boost to spending may not be sustained.

The UK rate of inflation, measured on a 12-month rate, has risen since the autumn. On the measure that includes housing costs (CPIH), inflation rose by 3.9 per cent in the 12 months to January, up from 3.5 per cent in the 12 months to December 2024.

However, month on month, there was little change. Excluding housing costs, the consumer price inflation rate (CPI) also accelerated to 3 per cent in the 12 months to January compared to 2.5 per cent in December 2024 although there was a small monthly fall.

The data reflects a modest slowdown in the rate of increase in housing and household services costs and more significant increases in the transport, food and non-alcoholic beverages and education sectors.

The latter includes an increase of 12.7 per cent in the price of independent school fees after the Christmas holidays compared to the previous term, reflecting the imposition of VAT at 20 per cent on private schools.

Housing and household services inflation fell between December and January on a 12-month rate as gas and electricity prices fell over the period.

However, owner occupiers’ housing (OOH) costs, which include the costs associated with owning, maintaining, and living in your own home including mortgage payments, rose in the 12 months to both December and January by 8.0 per cent – the joint-highest rate since February 1992.

The average purchase price of houses also continues to rise. In Scotland prices increased 6.9 per cent in the 12 months to December 2024, up on November (5.9 per cent) and above the UK average increase (4.6 per cent). The average price for a house in Scotland is £189,000 compared to £268,000 in the UK.

In contrast there was a modest slowing in the rate of increase in private rents, which rose by 6.2 per cent in the 12 months to January in Scotland, slower than the previous month (6.9 per cent) and the UK average (provisional estimate) of 8.7 per cent in January The average monthly rent was £995 in Scotland compared to £1,332 in Great Britain as a whole.

Despite these lingering inflationary pressures in the economy, the Bank of England is confident that these effects are temporary. After leaving interest rates unchanged in December, the Monetary Policy Committee cut interest rates by a quarter of a percentage point, to 4.25 per cent in February. The Bank now forecasts CPI inflation to peak at 3.7 per cent in the third quarter of this year before gradually returning to the 2 per cent target by the end of 2027.

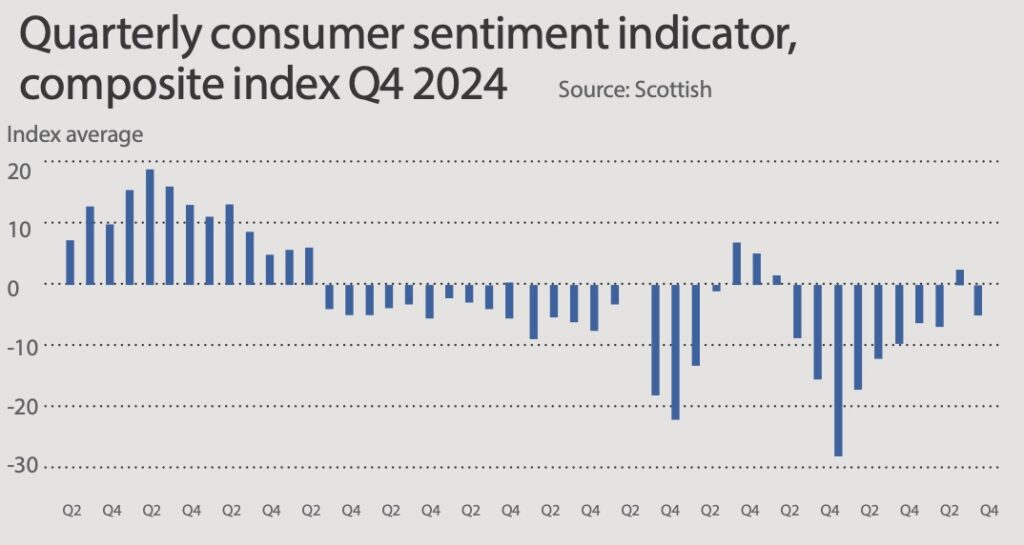

Weaker consumer sentiment did not stop shoppers enjoying the January sales.

Despite a positive return in the second quarter of last year, by Q4 2024, the Scottish Consumer Sentiment Index (in development data) was back in negative territory at -4.9, a drop of 4.7 points compared to Q3 2024. The weakening sentiment over the quarter reflects a drop in expectations for the economy, and to a lesser extent, personal finances, and spending over the coming 12 months.

Despite this weaker sentiment, data from the Scottish Retail Consortium suggests that shoppers took advantage of the January sales with sales rising by 2.2 per cent, adjusted for inflation, year-on-year. February’s shopper footfall data suggests however that this rise in sales volumes may not be sustained as footfall decreased by 0.3 per cent year-on-year in the month.

Business less positive about the economy

The latest Royal Bank of Scotland regional growth tracker, a seasonally adjusted index that measures the month-on-month change in the combined output of the region’s manufacturing and service sectors, showed a second consecutive but slightly shallower decline in business activity in Scotland in the January sales as new business orders fell and price pressures remained.

Only four UK regions or nations saw a positive expansion over the period. Looking ahead, while expectations of future business activity in January sales were positive across all parts of the UK, Scotland had the lowest score on this measure, perhaps because of greater relative uncertainty over future orders.

Firms responding to the Fraser of Allander Institute/Addleshaw Goddard’s Scottish business monitor in the final quarter of 2024 were also more downbeat. Most measures in the survey declined, including business activity by volume and sales, export activity and capital investment.

Cost pressures were a major concern for firms, with 94 per cent of respondents expecting higher business costs over the first half of 2025. Seventy-three percent of firms reported that the increase in Employer National Insurance Contributions from April will either have “a lot” or “a fair amount” of impact on their business operations.

Labour market stays resilient

The labour market remains resilient but challenging economic conditions are having an impact. According to HMRC PAYE data (which is subject to revision and reflects the home location of workers), the number of payrolled employees declined in Scotland over the 12-month period to January by 0.1 per cent (compared to an increase of 0.2 per cent in the UK overall).

This is the third consecutive month of flat or falling payroll employment Scotland on this basis. There were local bright spots, with Orkney boasting the highest payroll employment growth of any UK location at 2.8 per cent in the month of the January sales.

The claimant count for those unemployed and seeking work was 3.8 per cent in January, a modest increase on the previous month although this was still lower than the UK overall (4.6 per cent). Labourforce survey data also showed a slight increase in unemployment to 3.8 per cent in the final quarter of 2024 alongside a fall in the inactivity rate to 22.8 per cent and an increase in the employment rate (to 74.2 per cent).

The UK inactivity rate is slightly lower (21.5 per cent) whilst the employment rate is the same (74.9 per cent). This data should be interpreted with caution due to sampling constraints.

Recruitment indicators also indicate looser labour market conditions. New online postings of jobs in Scotland rose slightly in January but were down by 5.9 per cent compared to a year before (and relative to a decline of 16.3 per cent in UK figures).

However, this masks labour shortages in certain sectors with one in five Scottish employers still experiencing difficulties in hiring staff in January according to Scottish Government Business Insights and Conditions Survey (BICS) with the administrative and support services sector facing the most acute shortages (35 per cent) followed by health and social work (31 per cent).

Only 3 per cent of information and communications technology businesses are facing recruitment difficulties.

Median monthly pay increased by 5.2 per cent in the 12 months to January in Scotland (compared to 5.7 per cent in the UK), ahead of inflation and ensuring that real terms earnings remained positive.

Median monthly pay now stands at £2,486 in Scotland very slightly above the UK average (£2,467). However, earnings growth is expected to be weaker over the course of this year.

The Bank of England’s decision maker’s panel showed that, while annual UK wage growth was 5.2 per cent in the three months to January, anticipated wage growth for the year-ahead is only 4 per cent, which would still be slightly above forecast inflation for this year.

Scotland expands ahead of UK in 2024

Initial estimates (subject to revision) for GDP over the final quarter of 2024 indicate that the UK economy grew by 0.1 per cent, following no expansion in the previous quarter.

Growth was 0.9 per cent over the year. Growth in the services sector (0.2 per cent) and construction (0.5 per cent) in the final quarter were offset by a contraction in production (0.8 per cent). Preliminary data for January suggest a contraction of 0.1 per cent driven by a further contraction in production activity which included a drop in manufacturing, mining, and extraction of oil and gas.

In contrast Scottish GDP flatlined in the final quarter (0.0 per cent change) following growth of 0.4 per cent in the previous quarter. Over the year as a whole growth was 1.1 per cent up on 2023, slightly ahead of the UK. Final quarter growth was underpinned by the business, services and finance, and government and other services sectors while output in production declined by 1.1 per cent, slightly faster than the UK contraction.

Economists have updated their models to reflect the UK Government’s October budget. In December, the Fraser of Allander Institute forecast Scottish GDP will grow marginally faster at 1.3 per cent in 2025 (up slightly from September’s forecast) and by 1.2 per cent in 2026.

The Scottish Fiscal Commission was slightly more optimistic in December, forecasting growth of 1.5 per cent and 1.6 per cent respectively over the coming two years.

In February, the Bank of England halved its UK growth forecasts for 2025 to just 0.75 per cent but slightly upgraded its forecast for 2026 to 1.5 per cent.

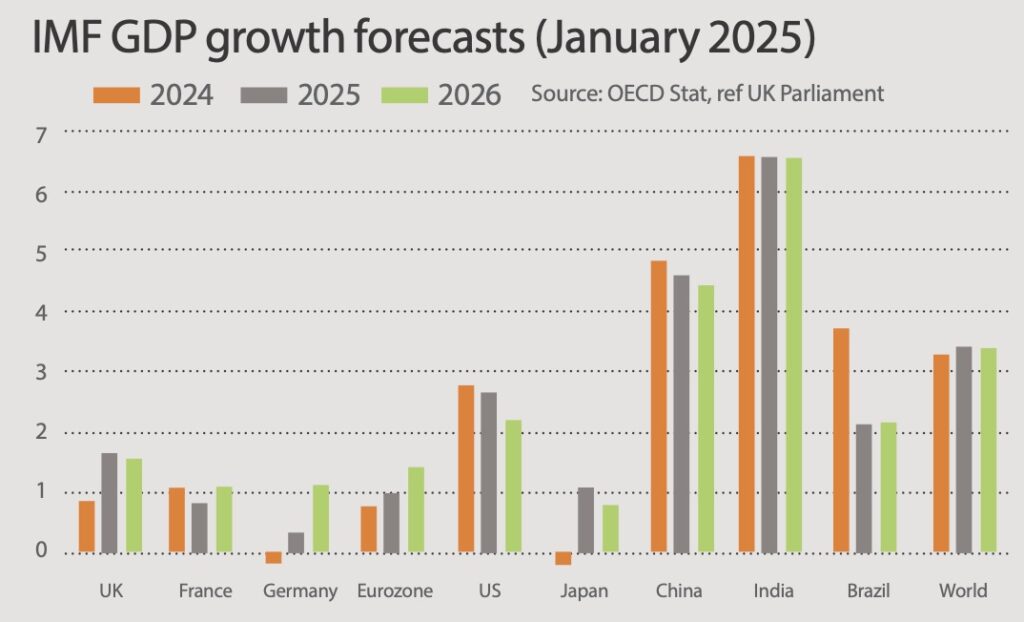

Putting this in an international context the updated January IMF (1.6 per cent) and December OECD (1.7 per cent) estimates for the UK are slightly more optimistic than the Bank for 2025 but still put the UK’s growth behind the US and ahead of France, Germany, and Japan.

Their forecasts for 2026 are for modest growth of 1.3-1.5 per cent in the UK. Analysis of the data since before the pandemic suggests UK GDP is now 3.2 per cent higher than at the end of 2019, the lowest rate in the G7 except Germany.