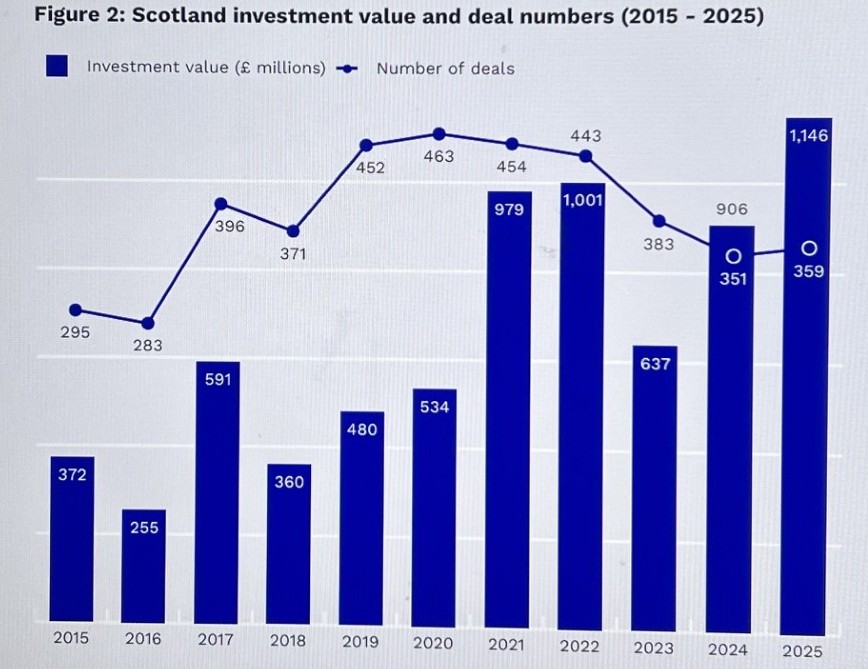

Scotland had a record-breaking year for investment value in 2025 — outstripping the post-pandemic peak years of 2021 and 2022. A total of £1.15bn was raised compared with £906m in 2024, a 26 per cent increase. However, a single megadeal of £445m into Edinburgh-based battery energy storage company Fidra Energy accounted for 39 per cent of Scotland’s total investment value.

Scottish Enterprise has published its latest Capital Market Report, entitled Investing in Ambition. Its benchmark analysis, based on Beauhurst data, shows while money invested in the UK is up 4 per cent to £24.39bn, the number of deals has dropped 7 per cent to 5,982. This contrasts with the picture in Scotland with the £1.15bn investment, which involved 359 deals, up 2 per cent. Nearly £200m, at £194m, was invested in Scottish spin-outs, which represents 17 per cent of the total.

Derek Shaw, the Director of Entrepreneurship and Investment at Scottish Enterprise, the national economic development agency, believes the results are a strong indicator of Scotland’s investment potential.

“The key takeaway from the 2025 report is the not insignificant increase overall in the level of investment at £1.15bn, which is a 26 per cent increase on 2024 figures. This is notwithstanding the fact that one particular deal was a very large deal and contributed £445m. This is very encouraging for Scotland, but we can’t rest on our laurels,” he says.

“We have three inter-linked missions at Scottish Enterprise. We want to accelerate the energy transition creating competitive international companies in Scotland; we want to scale our innovation with high-growth firms of the future; and we are seeking to boast capital investment which will make major improvements in Scotland’s productivity,” continued Shaw (pictured below).

If Scotland wishes to scale-up more companies, the size of single investment on deals has to increase to over £10m, and increasingly in the plus £50m to £100m category. While megadeals, of over £100m, are an important feature of global risk capital value in 2025, there has been only one in Scotland.

The Fidra Energy sale is an interesting case because of the company’s creation and evolution. Fidra was established in 2021 by several experience executives involved with West Burton Energy, which was sold to Total Energies in 2024. They pulled together their massive industry experience and coupled this with major international support from capital markets to supercharge their growth.

Fidra’s money from the National Wealth Fund and US corporate investor EIG Partners, is allowing the company to complete the financial closure of the UK’s largest energy storage system (BESS) project at Thorpe Marsh in Doncaster, South Yorkshire. Thorpe Marsh is expected to be three times larger than any other BESS project in the UK with potential to export over 2 million MWh annually, positioning this Scottish headquartered company as a global competitor.

KEY ROLE FOR SCOTTISH ENTERPRISE

Derek Shaw sees Scottish Enterprise’s role as helping high growth companies at each stage of the investment cycle.

“If you look at the spread of investment from early stage from £2 to £10 million, and then £10m and above, it is positive. We need to ensure early-stage companies continue to be supported and that there is a raft of investors keen to be involved with early-stage, spin-out opportunities.”

Scotland’s risk capital landscape continues to attract a range of investor types. Venture Capital (VC) and Private Equity (PE) investors remain active in the Scottish market, despite decreases in the value and volume of participations.

Individual business angels and angel syndicate networks also played an active early-stage role in the Scottish market. Angel networks in Scotland were the most active in the UK for both value and volume of participations. Scottish Enterprise has been able to double the investment in many cases by backing the angel networks on a pound for pound support.

“Then, as Scottish companies grow and scale, that requires access to the later rounds of investment that they need in the £10m and above category, with this a key threshold. We are looking at the overall picture. When you look at VC investment, in particular, we had around 80 deals in Scotland. I think that’s positive. We’re seeing more international investment coming through,” says Shaw.

Shaw is also encouraged that Scotland was the top performing nation and region outside the ‘Golden Triangle’, of London and East of England, ranked fourth for deal count, rising from sixth place. Scotland was the only part of the UK to see both investment value and number of deals increase in 2025.

The major 2025 Scottish deals, according to the analysis, were:

| Company | Value |

|---|---|

| Fidra Energy | £445m |

| Trogenix | £70m |

| Orbex | £55m |

| BLK | £50m |

| Chemify | £37m |

| Invinity Energy Systems | £25m |

| Wordsmith | £18.5m |

| Argyll Infrastructure Holdings | £15m |

| Cruden | £15m |

| IONATE | £13.8m |

| iGii | £11.7m |

| Kelso Pharma | £11.7m |

| Central Plains Group | £11.4m |

| Highland Broadband | £10m |

Shaw continues: “So companies, such as Trogenix, a clinical stage spin-out in biotechnology from Edinburgh University, which is using machine learning, has Series A level funding of £70m. While Chemify, from the University of Glasgow, spin out at the intersection of biotech, AI and digital biochemistry, has Series B level of funding, at over £37m. That’s fantastic and I think it’s testament to the quality of innovation coming out of Scotland and particularly from our universities.”

“I think it’s also great testament to those management teams that have identified those investors and brought those investors into those businesses,” he added.

Wordsmith is the fastest-ever Scottish start-up to reach a valuation of over $100m, achieving this just 18 months after its launch. The company is dedicated to helping build an AI ecosystem in Scotland for the legal profession.

One potential trouble spot is that deals worth £10m and above would have declined if not for Fidra Energy.

“The importance of growth in the market below £2 million should not be overlooked. This band usually includes companies at the earliest stages of their investment journey, who could go on to scale and potentially attract investment of £10 million and above in the future,” said the report.

Despite these strengths, challenges remain in the global risk capital market, to which Scotland is not immune. The report stated: “Exit volume remained subdued in 2025, highlighting the continued struggle to return capital to investors. The fundraising environment has become more difficult for companies, with valuations falling at the early-stages and strong metrics and profitability of greater importance than ever to increasingly selective investors.”

“Many struggle to demonstrate a track record, lack collateral, or are simply unaware of their finance options. These challenges have an even more fundamental impact on under-represented groups seeking investment,” it added.

The data also shows that predominately female founded companies accounted for the lowest proportion of total investment value and deals in Scotland, despite improved overall performance in terms of average deal size, investment value and deal count in 2025.

Another encouraging aspect is the number of companies new to equity investment value is increasing. At a UK level, new to equity investment value grew by 21 per cent from £3.85bn to £4.66bn. The percentage increase was far greater in Scotland, up by 188 per cent from £181m to £522m.

Without the Fidra deal, new to equity investment value would be £77m (57 per cent less than in 2024). Additionally, this deal makes new to equity investment account for almost half of all Scottish investment in 2025. The majority of new to equity investment raised in 2024 was also made up by just one deal (£45.1m into Aberdeen-based CRC Evans). There no new to equity deals on the scale of either of these deals in Scotland, even in 2021 or 2022, when valuations were particularly high.

THE SEARCH FOR VENTURE BUILDERS

Scottish Enterprise sees its role in continuing to support the pipeline, working with the universities.

“We are looking at is how we bring on the ‘Venture Builders’. This is about ensuring we are bringing in the commercial, industry expertise at the very early stages of a proposition so that for people that have been there and done it before, and know the size of the market opportunity and the technology, and often with all due respect to our first time founders and our scientists and our academics, who are fantastic at innovation.”

“But where we really need support is around that market opportunity, the scale of the market opportunity. So what we are looking at is what does a Venture Building model look like for Scotland?”

He says this is happening in England, with Northern Gritstone and Cambridge and Oxford who have got venture building models. What would a successful model look like for Scotland to really support more companies to scale globally, for those hyperscale opportunities. So taking the best of what’s coming out of the universities, providing the wraparound support in a way that complements and augments and accelerates what we’re doing just now, but also provides that funding to enable those companies to be a success.”